Just like a human body goes through different stages of life such as infancy, childhood, adolescence, adulthood, and old age, your finances also encounter the same fate. Financial planning is of paramount importance, but is it a one-time thing? The answer is No. The two major aspects of financial planning are income and expenditure, which differ age to age. In addition to that, the financial goals also vary at different ages, like you do not wish for a sea facing duplex at the age of 25, unless your last name is Zuckerberg. So what exactly are these financial life stages and how one can plan them?

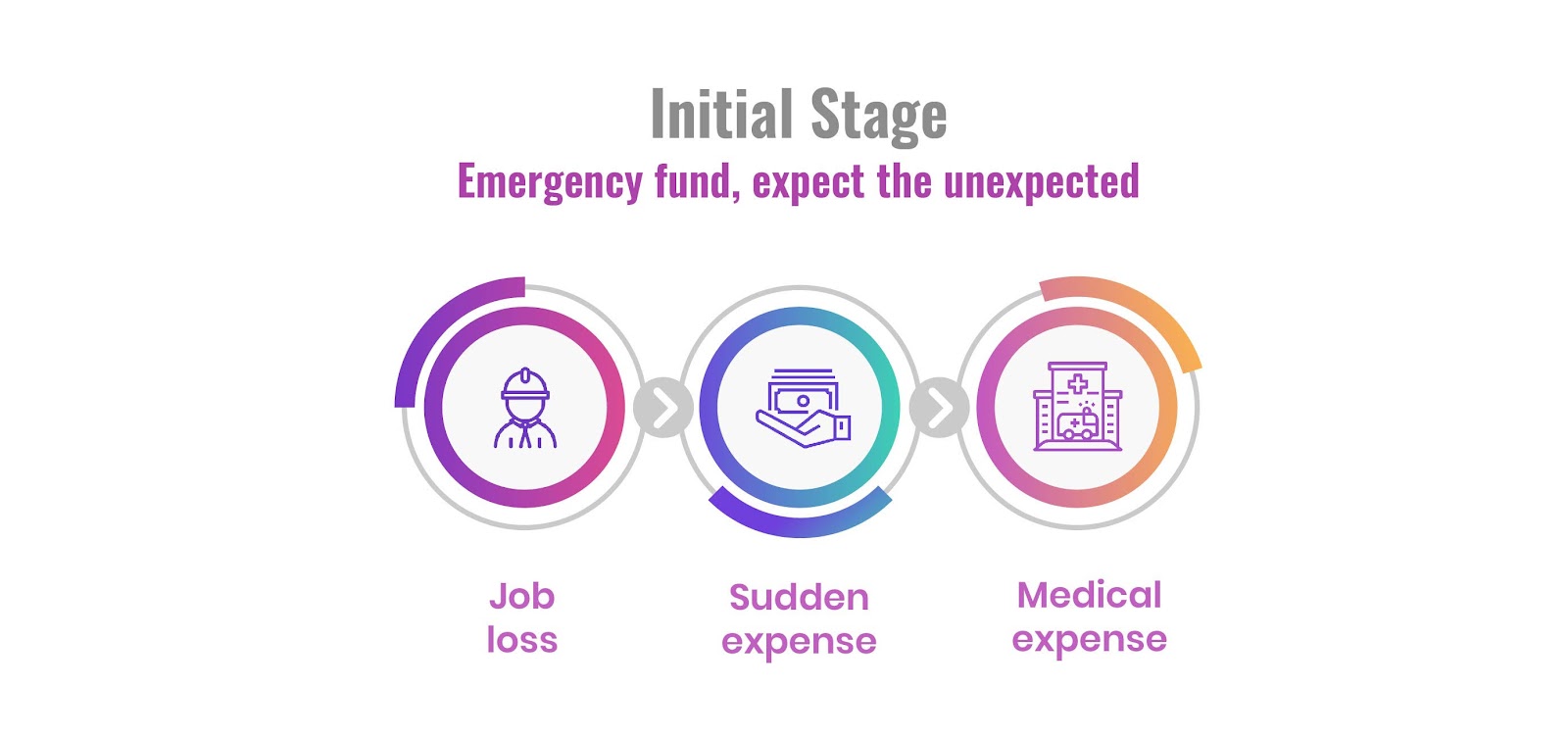

Stage 1. Just like infancy, this stage is very premature for decisions like savings or investments, however in case of financial planning, the earlier the better. In this stage the income side has begun to tick, but at a considerably lower rate, but if we control our urge to avoid unnecessary expenses, the expenditure restrictions later may not be required. The first and foremost necessity in any stage is building an emergency fund and then maintaining consistency for the same. Things like term insurance may be ignored, unless you are the only earning member, although a basic mediclaim policy may come handy for the family. The investment perspective can be thought, once you figure out the monthly savings amount. Therefore in this stage main concentration should be on savings and creation of emergency fund.

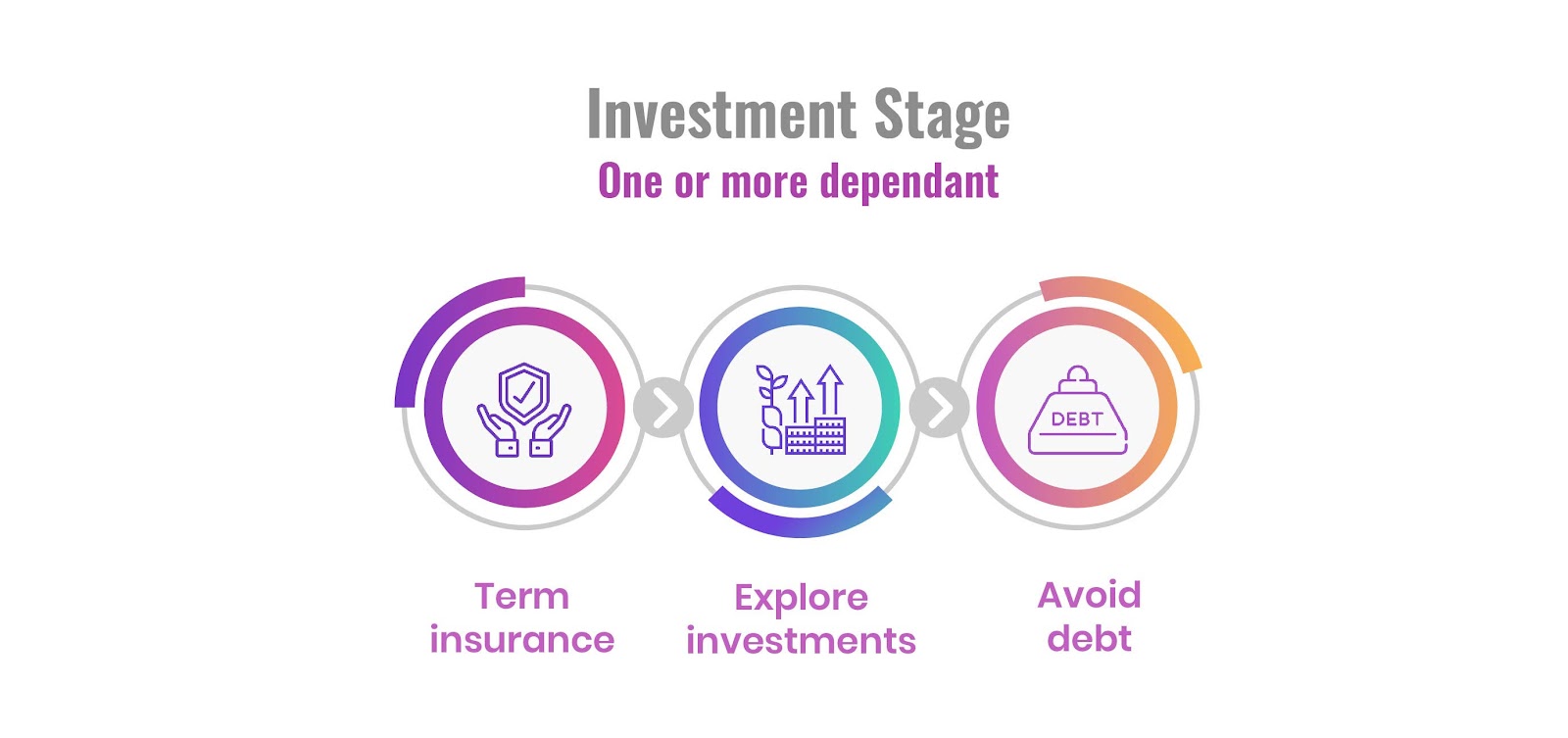

Stage 2. This stage comes into picture mostly after your marriage or parents retirement, where the dependency upon you is on the rise. As a result term insurance becomes a sudden necessity. At this stage, one may want to spent more than his/her earnings, paving way for debt, therefore management of credit card bills, and avoidance of unnecessary interest cost must be avoided. Investment scenario is opened and must be explored at this stage, but without disturbing the emergency fund and term insurance or health insurance expenditure. Investment opportunity must be properly studied, and giving regards to returns, liquidity and tax benefits the most suitable one must be picked.

Stage 3. This is the stability phase, where all your expenses, savings and investment are properly allocated. A general review is essential, and the flexibility muscles must be put to use in order to achieve better returns. The expenses again must be made after giving due regards to savings, where savings first moto should always be adopted. The insurance must also be given a check, and changes to be made according to necessity. Since the income at this stage of financial life is at all-time high, it should not be the case of excessive spending. As dependents such as children, will eat up considerable amount of your savings in their educational expenditure. The ultimate financial goals such as retirement fund or buying a house, should never be sacrificed, as only consistency in planning can help you achieve them.

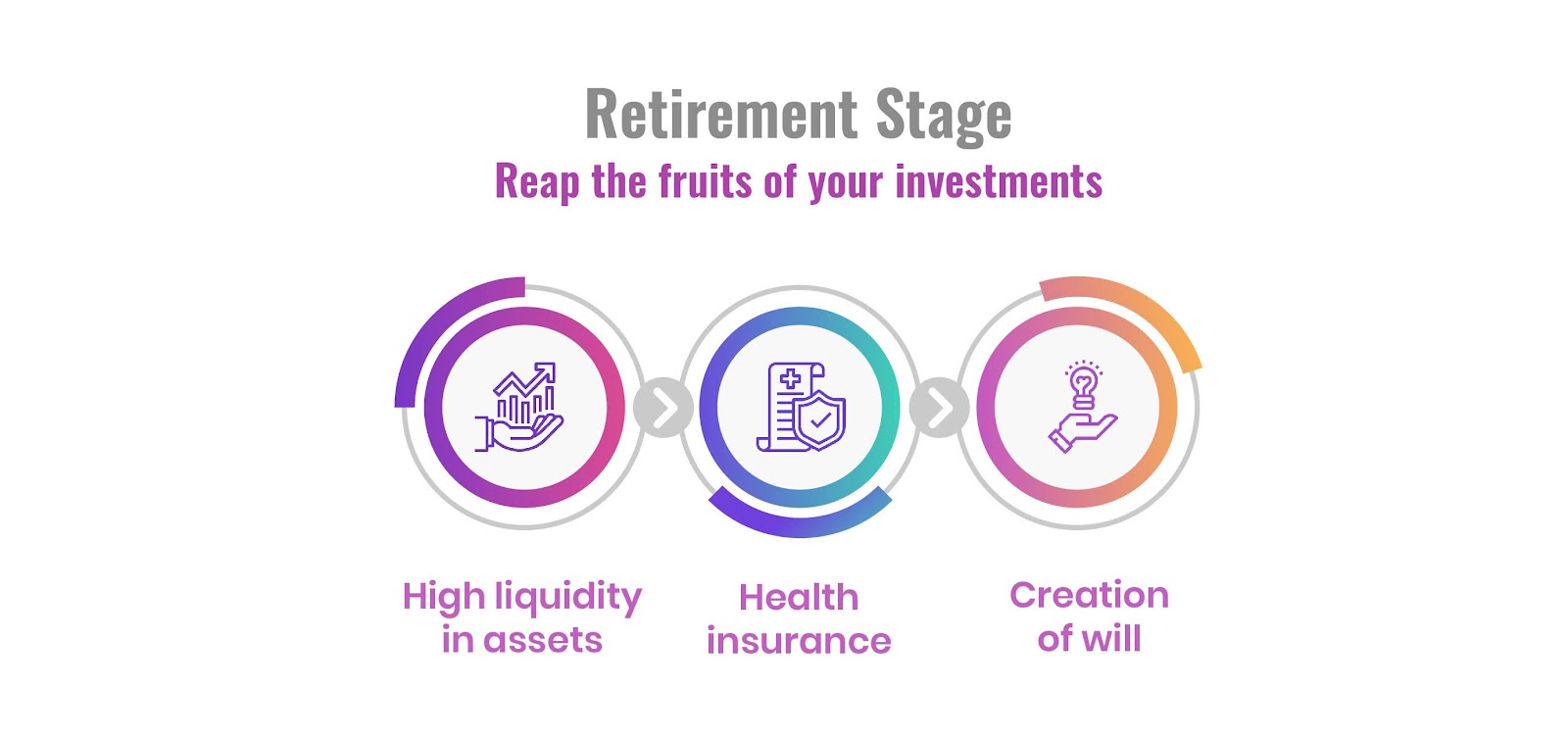

Stage 4. The final stage of financial planning, where the seed rowed at the beginning must now come to fruition. The income side here might not be as strong and may depend heavily upon pensions, thus expenses must be kept within them. Debt at this stage is big no, since the income source are scarce and serving interest will be big ask on low income. Health insurance is an absolute must at this stage and the policy which gives you maximum coverage must be chosen. Life insurance will become costly due to the age criteria, hence can be avoided unless, deemed necessary to secure spouse’s income. Investment with high liquidity and low risk can be preferred. Creation of will is also necessary part of financial planning, in order to avoid the litigation amongst descendants. No money is sufficient money at this stage, but something is better than nothing.